What is Tokenization and How are Banks Tapping Into its Design Principles?

- Tokenized Commodities Council

- Nov 30, 2022

- 6 min read

Originally posted by COINTELEGRAPH on Dec 01, 2022.

Financial services organizations can use tokenization to solve several friction points and have better risk management in place.

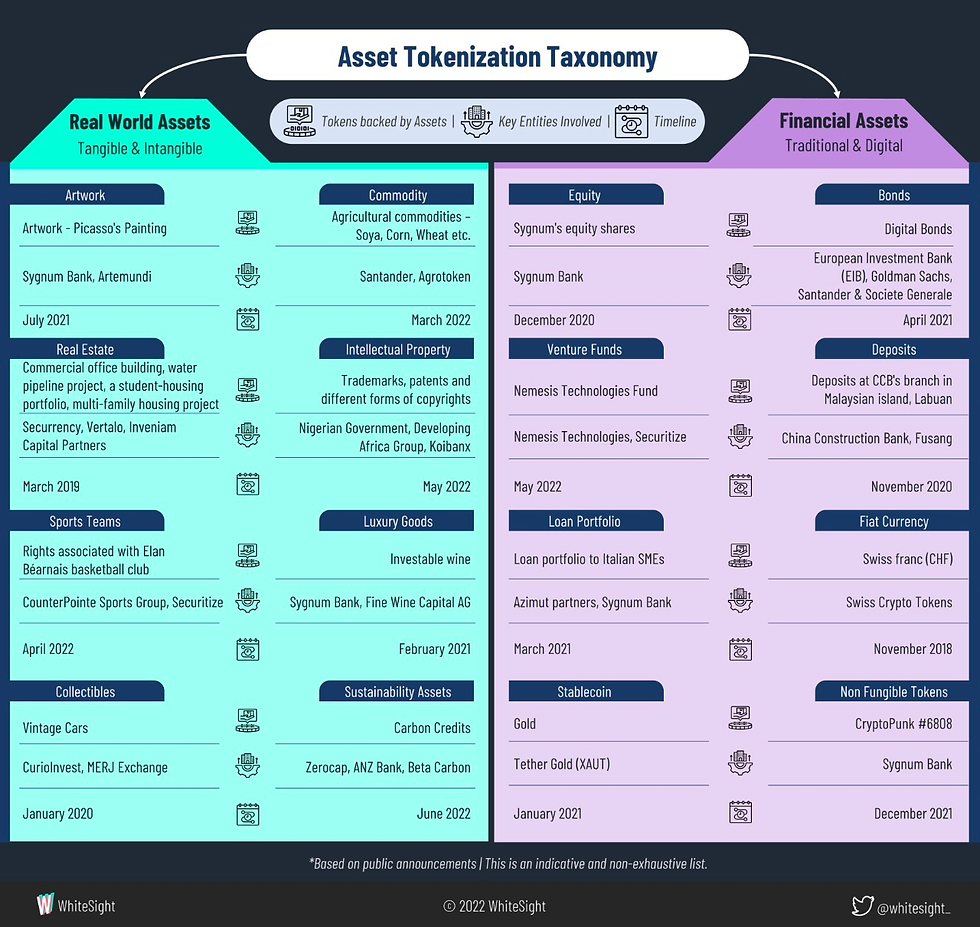

Tokenization is the process of converting something with tangible or intangible value into digital tokens. Tangible assets like real estate, stocks or art can be tokenized. In a similar vein, intangible assets like voting rights and loyalty points can be tokenized, too. We see Avios as an example of tokenized loyalty points by the traditional credit card industry.

However, when tokens are created on a blockchain, they add a level of transparency that previous iterations of tokens couldn’t achieve. There are several banks that are experimenting with tokenization. But, before diving into the use cases in banking, it would be useful to understand the qualitative advantages that tokenization brings to financial services.

As major financial institutions enter the crypto space, they pay special attention to issues like custody and Anti-Money Laundering analytics and compliance. Now, with the dramatic collapse of FTX, the key qualitative benefits of tokenization are in the spotlight yet again.

Liquidity

Real estate is one of the most illiquid asset classes. When a property is worth a few million dollars, buying and selling the property can take time. Now, imagine a $1 million home is tokenized, with each token representing property ownership. When these tokens are available for purchase in the market, 100 buyers can each invest $10,000 to buy ownership of the property.

This naturally increases the ease with which illiquid assets can be sold, as fractionalized ownership is possible with tokenized assets. Fintech firms like Yielders already implement fractional ownership of real estate without using blockchain tech. Also, illiquid asset classes like private equity and venture capital can benefit from tokenization.

When an illiquid asset like real estate or art is tokenized, the entire asset class benefits from the liquidity created. It also allows for a healthy secondary market and creates more data for better valuation of these assets. Platforms like Reinno and Realt offer global investors access to tokenized real estate.

As a property owner, this opens up options of selling just part of the property through tokens instead of selling the entire property. From an investor perspective, someone in Brazil with $1,000 can invest in property in Manhattan.

For instance, Realt offers investors tokenized properties. While the properties listed on their platform cost from several hundred thousand dollars to a few million, they are tokenized and each token can be valued at less than $50. This makes it extremely affordable for interested investors in most places of the world.

Similarly, fractional ownership of nonfungible tokens (NFT) is being rolled out for the more expensive NFT and art collections. As a result of a liquid secondary market for an illiquid asset, pricing also becomes easier due to transparent supply and demand dynamics.

Liquidity risk management

In addition to these benefits, liquidity risk management within financial services organizations can also benefit from tokenization. That benefit is a lot clearer from the FTX collapse and how tokenization could have helped there.

The FTX collapse had several underlying issues, not the least of which came from its business model using the volatile FTX Token FTT $1.90 as collateral. However, if there were checks and balances in place that were transparent for customers to see, mitigating actions could have been taken in time.

At no point in their journey did FTX create transparency around how much liquid assets they had to service their liabilities. As a result, FTX managed to repurpose user funds (liabilities) for their investments (illiquid assets). Tokenizing both assets and liabilities would have shown a liquidity gap in real-time and cautioned the market of the looming crisis.

After the FTX collapse, there has been a rushed effort to provide proof of reserves from several centralized crypto exchanges. However, proof of reserves only shows that a firm has some assets to service its debts.

An equally important capability is proof of liabilities. If a firm can transparently demonstrate that it has $1 billion in reserves/assets, but its liabilities, which could be $10 billion, are not clear for everyone to see, its solvency is under question.

The challenge in creating transparency around liabilities is that, often, firms capitalize themselves through debt raises in fiat currencies. As these instruments are not tokenized, real-time solvency cannot be demonstrated. Therefore, in order to avoid an FTX-like incident in the future, exchanges will need to provide proof of assets and liabilities.

One of the key qualitative aspects of tokenization that is apparent from the FTX saga is the “proof of solvency.” The transparency that tokenization brings can also help assess the solvency of a firm in real-time. If both assets and liabilities of a bank can be tokenized, on-chain analytics can be used to understand if the firm has enough assets to service its liabilities.

Democratization

The tokenization of assets makes them more accessible to retail investors. In the example given earlier, an investor with $10,000 could own a share of a million-dollar property in a prime location and benefit from a rise in its value. Without tokenization, they wouldn’t be able to participate in big-ticket assets that offer good returns.

This is particularly true with high net worth individuals who want access to products that are only available for private banking clients. In the past, products with attractive returns profiles were offered exclusively to institutional investors. Even high-net-worth and sophisticated investors would struggle to get access to these assets.

Efficiency

As financial services firms and banks tokenize their asset base, the instant finality that blockchain offers can help them see where they stand with their capital health in real-time. Settlements which used to take two days, referred to as (T+2), can now be instant. This offers both operational and capital efficiencies.

Organizations can assess their precise level of capitalization and make quick and profitable decisions to deploy their capital. In times of market crisis, the same capability can help manage capital and reduce risks.

With all these purported benefits, what are banks and financial services firms experimenting with tokenization?

JPM Coin

JPM Coin is JPMorgan’s version of a United States dollar stablecoin. JPM Coin is currently in its prototype stage and is being trialed and tested for money transfer across JPMorgan’s institutional customers. JPM Coin may be launched in other currencies should the dollar prototype prove successful.

As described by the bank, institutions that participate in this exercise typically follow a three-step transaction process.

Institutions open a deposit account with JPMorgan and deposit USD in it. They receive an equivalent amount of JPM Coins.

Institutions can transfer JPM coins globally to other institutions that are JPMorgan clients. This can be just a currency transaction or a security transaction paid in JPM Coins.

The recipient institution can redeem JPM Coins for USD.

Regulators are yet to approve JPM Coin. Only after comprehensive regulatory approval is obtained can it launch for retail use.

The Depository Trust and Clearing Corporation (DTCC)

The DTCC is a U.S.-based organization that acts as a centralized clearing and settlement company for different asset classes.

In Q4 2021, the DTCC announced a platform to streamline the issuance, transfer and servicing of private market securities through tokenization. Apart from implementing the platform, they also provide a common market infrastructure and standards across private market assets.

As discussed in the qualitative aspects of tokenization, asset classes like private equity and venture capital can be quite illiquid and inaccessible. As a result, the secondary market for private securities is quite nascent.

Tokenizing these securities and providing market standards could help improve liquidity within these asset classes and also help with efficiencies in settlements. The DTCC has started with the Ethereum blockchain, but the platform can be blockchain agnostic. It plans to offer both public and private blockchain support based on market demand.

ADDX

ADDX is a Singapore-based blockchain startup that is currently pioneering efforts in tokenizing private market securities for which both accredited investors and institutional investors are eligible to participate.

Assets include venture capital funds, private credit funds, real estate funds, ESG bonds and more. Access to such institutional investment vehicles was limited to a select few in the past. Thanks to fractional ownership through tokenization, accredited investors with a net worth of 2 million Singapore dollars ($1.47 million) can participate in these assets.

The end of banks?

Some claim that digital assets and Web3 are going to be the end of banks, but it is unrealistic to expect that such financial institutions will be relegated to the past. And yet, while banks are likely to remain strong, banking as we know it today is likely to change for the better.

There are several elements of banking that could undergo operating and business model changes over the next couple of decades, largely inspired by digital assets and their underlying design principles.

Comments